The Fraud Threat Lenders Can No Longer Outrun with Rules Alone

Fraud is no longer a static problem. The schemes targeting lenders today — synthetic identities, account takeovers, coordinated fraud rings — are built and adapted using the same AI tools that financial institutions are only beginning to adopt for defense. The gap between attacker sophistication and institutional readiness is widening, and static rule sets are bearing the cost.

For years, lenders have relied on threshold-based fraud rules: flag a transaction above a certain amount, block a login from an unfamiliar device, hold an application when the address doesn't match. These rules were built for yesterday's fraud, and they are fighting tomorrow's. Fraudsters study rule sets. They calibrate attacks to fall just below thresholds. They rotate device fingerprints. They apply synthetic identities that pass individual rule checks while hiding coordinated behavior at the portfolio level.

AI fraud detection for lenders addresses this challenge not by adding more rules but by replacing the paradigm entirely — moving from static response to continuous, adaptive learning. Lenders who understand how to deploy AI-driven fraud intelligence, and how to pair it with the human judgment and collaborative networks that remain irreplaceable, are building defenses that get stronger as fraud evolves. Lenders who wait are building a gap that compounds.

Lenders running compliance and identity workflows inside Salesforce can integrate AI fraud signals directly into their decisioning layer — so alerts don't live in a separate system that no one checks.

So what does this mean for your institution? Fraud losses are not just a security problem — they are a compliance problem, a capital problem, and increasingly, a regulatory examination problem. The time to evaluate your fraud detection architecture is before an examiner asks why you missed the pattern.

What AI-Driven Fraud Detection Actually Does Differently

Traditional fraud systems answer a fixed question: does this transaction match a known bad pattern? AI fraud detection asks a different question: does this behavior deviate from what is normal for this account, device, identity, and context — right now?

That shift matters because fraud patterns are not fixed. The organized fraud rings targeting lenders today operate with operational discipline: they test attacks, refine methods, and move on when detection rates rise. A rule-based system requires a human analyst to observe the pattern, write the rule, and deploy it — by which time the attack has already evolved. AI systems observe behavior continuously and update their models in real time. A fraud network that successfully evaded detection last week will be generating anomaly signals this week without any manual intervention.

The most operationally significant capability is device intelligence. Modern AI-driven fraud tools build unique device profiles from a large dataset — IP addresses, browser configurations, behavioral biometrics, session timing, and dozens of additional signals — and compare incoming behavior against those profiles in real time. A new account application that arrives from a device profile associated with 14 prior declined applications at other institutions is flagged immediately, even if every individual data point passes manual review.

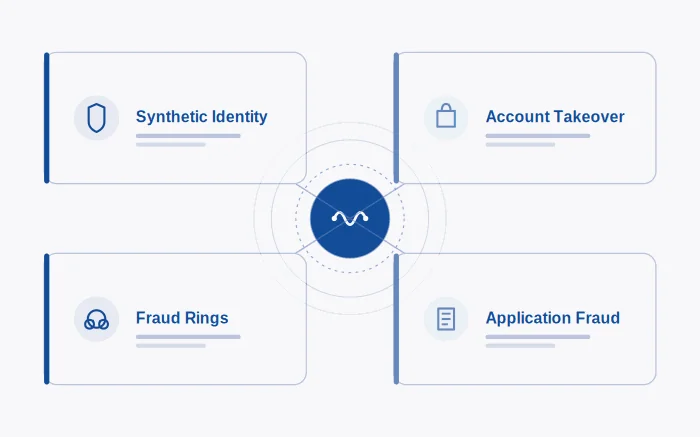

This is especially critical for detecting the two fraud types that continue to cost lenders the most: synthetic identity fraud and account takeover. For a deeper look at how synthetic fraud is constructed and what detection signals to prioritize, see our overview of synthetic identity fraud detection.

| Fraud Type | Why Rules Fail | What AI Detects |

| Synthetic Identity | Each individual data element may be valid | Behavioral pattern inconsistencies across applications |

| Account Takeover | Attacker uses valid credentials | Device profile anomalies, session behavior deviations |

| Organized Fraud Rings | Ring members don't share obvious attributes | Cross-portfolio clustering and timing correlations |

| Application Fraud | False data passes static field validation | Velocity signals and identity consistency gaps |

So what does this mean for your institution? The fraud types most likely to generate significant losses — synthetics and organized rings — are precisely the ones that rule-based systems are structurally unable to detect. Investing in AI-driven detection is not optional for lenders who originate at volume.

How Better Fraud Detection Connects to Lender Business Outcomes

It is tempting to frame fraud detection as a cost center — a defensive investment with no revenue upside. That framing is wrong, and lenders who accept it tend to underinvest until a loss event forces a reckoning.

AI fraud detection generates measurable business outcomes across three dimensions. First, it reduces false positives — the legitimate applications and transactions that static rules incorrectly flag as suspicious. False positives cost lenders real money in manual review hours, and they cost institutions members and borrowers who abandon applications that get stuck in friction. A system that accurately distinguishes genuine anomalies from edge-case legitimate behavior reduces that friction without reducing security.

Second, AI-driven detection enables faster response. The mean time between fraud event and detection is one of the most consequential variables in loss exposure. Systems that flag anomalies in real time and route them to human reviewers through a structured alert workflow — rather than generating batch exception reports overnight — compress that window from days to minutes.

Third, and most importantly for lenders with growth ambitions, effective fraud infrastructure enables digital origination at scale. The fraud risk in digital account opening has increased substantially alongside volume — as documented in rising fraud rates across digital channels. Lenders who can open accounts and originate loans digitally without a proportional increase in fraud losses have a structural competitive advantage. Those who cannot are limited to origination volumes their manual review capacity can handle.

So what does this mean for your institution? Fraud detection infrastructure is not just a defense investment — it is an enabler of digital growth. The lenders who will win the next five years of volume expansion are the ones whose fraud systems can scale with them.

Ready to see how LASER handles fraud detection and compliance natively inside Salesforce? → Schedule a Discovery Call

What the Data Says About Fraud Risk and Detection Gaps

Fraud is not a theoretical concern for lending institutions. The data is specific, the losses are documented, and the regulatory attention is increasing.

North American identity fraud losses have reached $47 billion annually, a figure that reflects not just direct losses but the downstream compliance, remediation, and reputational costs that accompany each incident. Account takeover fraud, which leverages valid credentials obtained through phishing, social engineering, or data breach exposure, has accelerated alongside digital channel growth. The Justice Department's seizure of a fraud domain connected to a $28 million bank account takeover scheme is one of the more visible enforcement actions — but the cases that don't generate DOJ press releases are far more numerous. The pattern across lending institutions is consistent: the fraud risk in digital account opening is rising in direct proportion to volume.

Industry collaboration has emerged as a meaningful force multiplier for institutions that participate. Fraud rings rarely target a single institution — they move systematically across portfolios, testing and refining methods. Specialized intelligence-sharing groups — closed communities that connect lenders, issuers, merchants, and law enforcement — give members early warning of emerging attack patterns before they generate losses. Fintech partners are also advancing detection at the call center level, where voice authentication and enhanced identity validation are closing a gap that has historically been difficult to address through data signals alone.

In our work with commercial lenders, the institutions with the strongest fraud postures share a common characteristic: they treat fraud intelligence as a live operational input, not a quarterly report. They know their current false positive rate. They know their mean detection time. And they have a clear line between their fraud alert system and the human reviewers who act on it.

So what does this mean for your institution? Fraud intelligence that lives in a system your team doesn't review in real time is not fraud intelligence — it's a compliance liability. The gap between detection and response is where losses happen.

What Lenders Should Do Next: A Practical Fraud Detection Framework

Addressing fraud detection gaps does not require replacing every system at once. The most effective path forward follows a structured sequence — assess current state, close the highest-exposure gaps, build toward integrated detection.

Step 1: Audit your current detection architecture. Map which fraud types your existing rules address and which they don't. Synthetic identity and organized ring detection are the most common gaps. If your current system generates batch exception reports rather than real-time alerts, that alone is a material exposure.

Step 2: Evaluate AI-driven tools against your highest-risk channels. Digital account opening and call center interactions are the two channels where AI fraud detection delivers the most immediate ROI. Device intelligence and voice authentication address the fraud vectors that are most active in those channels.

Step 3: Establish a human review protocol for AI-flagged alerts. AI detection generates signals — humans make final determinations. A structured alert management workflow that routes flagged cases to reviewers, tracks resolution outcomes, and feeds those outcomes back into the detection model is essential. The feedback loop is what makes AI fraud systems improve over time.

Step 4: Participate in fraud intelligence networks. Closed industry groups that share threat intelligence across institutions provide early warning that no individual institution's data can replicate. The investment in participation is modest; the intelligence return is significant.

Step 5: Align fraud detection with your compliance and decisioning workflows. Fraud signals that live in a siloed system separate from credit decisioning create operational gaps. Institutions that integrate fraud detection with their loan origination and identity verification workflows respond faster and with greater accuracy.

So what does this mean for your institution? A sequenced approach turns fraud detection modernization from an overwhelming infrastructure project into a series of achievable operational improvements — each of which delivers measurable return before the next step begins.

Why LASER for AI Fraud Detection

Fraud detection only performs as well as the system it's connected to. For lenders operating on Salesforce, the most operationally significant question is not which fraud tool to evaluate in isolation — it's how fraud intelligence integrates with the credit access, compliance, and decisioning workflows that already run your institution.

LASER Credit Access is built for exactly that integration. Salesforce-native credit access, built-in compliance, and decisioning — unified in a single app, ready from day one. Fraud signals, identity verification, and compliance alerts surface inside the same Salesforce environment where your team manages relationships, reviews applications, and tracks loan performance. There is no separate login, no manual data transfer, and no gap between a fraud flag and the decisioning workflow it should inform.

LASER's integration with Plaid enables identity verification and data aggregation directly within the Salesforce workflow — so the verification steps that matter most in fraud prevention happen in the same environment as the credit decision. Learn more about how LASER's Salesforce-native compliance layer works and explore how the platform handles fraud risk in digital account opening.

To learn more about LASER Accuracy, LLC and Michael Dunleavey's background in credit infrastructure and lending compliance, visit our About page.

Ready to Build Fraud Defenses That Strengthen as Threats Evolve?

AI fraud detection for lenders is not a future capability — it is a present competitive requirement. The institutions that combine real-time AI intelligence with structured human review, collaborative threat sharing, and integrated decisioning workflows are already compressing their detection windows and reducing their loss exposure. The institutions that don't are absorbing losses that their fraud reports may not yet fully reflect.

The most practical next step is a conversation about where your current fraud architecture has gaps and how Salesforce-native detection and compliance tools can close them.

Source: Staying ahead of evolving fraud: How AI and collaboration strengthen credit union defenses, CUInsight.